The Q3 2025 period (July through September) provides a useful snapshot of the current darknet market ecosystem. This research summary aggregates data from publicly available monitoring services, blockchain analysis, and community-published market metrics to characterize the state of the sector. All figures should be treated as estimates subject to the inherent limitations of darknet market research.

Overall Market Activity Trends

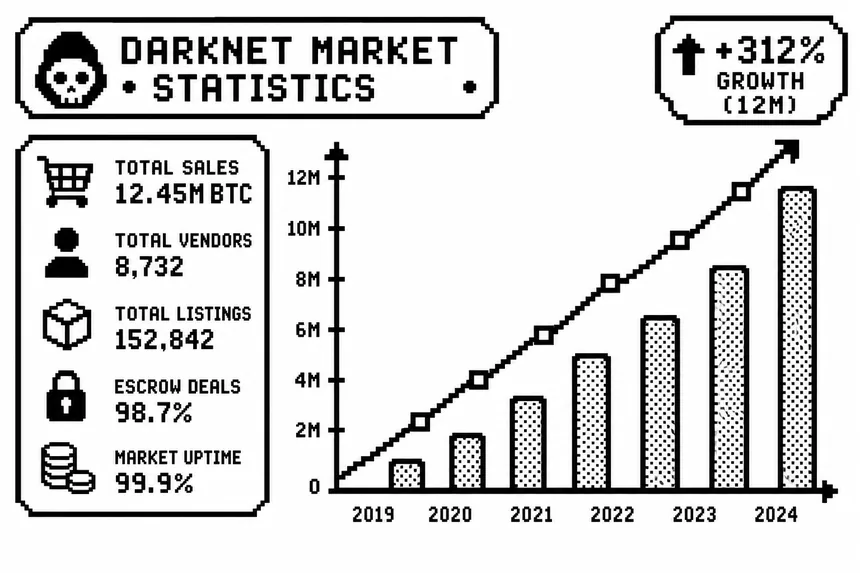

Q3 2025 saw continued growth in darknet market activity relative to the comparative period in 2024. The consolidation pattern observed since 2022 — where a smaller number of larger, more technically mature markets capture an increasing market share — continued. Markets with established reputations and documented security track records significantly outperformed newer entrants in terms of vendor onboarding and transaction volume.

Law enforcement activity in Q3 was below the elevated levels seen in Q1 and Q2, contributing to a more stable operating environment for established platforms. No major seizures were documented during the quarter, though several smaller platforms ceased operations voluntarily or through exit scam events.

Cryptocurrency Payment Method Analysis

Payment method preferences shifted further toward Monero during Q3. Based on data from markets that publish aggregate payment statistics and blockchain analysis of known market wallet clusters:

| Payment Method | Q3 2025 Share | Q3 2024 Share |

|---|---|---|

| Monero (XMR) | 68% | 57% |

| Bitcoin (BTC) | 24% | 36% |

| Other / Hybrid | 8% | 7% |

The 11-point increase in XMR share over 12 months is consistent with the trend observed since 2021. Several markets that previously supported only BTC added XMR support in the intervening period, while two markets removed BTC support entirely to streamline operations and reduce blockchain analysis exposure.

Escrow System Performance

Markets with documented escrow implementations reported escrow success rates (orders completing without dispute) of approximately 94-97%, consistent with prior quarters. Dispute rates averaged around 3-5%, with approximately 1% of total orders resulting in formal arbitration. Vendor-against-buyer fraud disputes represented a small fraction of total disputes, suggesting that reputation-weighted feedback systems continue to function as fraud deterrents.

Finalize Early (FE) transactions — where buyers release funds before receiving goods — represented approximately 8% of volume, down from 12% in 2023. This decline reflects both increased user education around FE risks and platform policy changes that restrict FE access to vendors above trust threshold levels.

Vendor Registration Trends

New vendor registrations across tracked markets increased by approximately 15% in Q3 2025 relative to Q3 2024. Bond requirements, which serve as fraud deterrents, ranged from 0.05 XMR to 0.3 XMR across platforms, with higher-reputation markets tending toward higher bond requirements. Vendor retention (vendors completing more than 10 transactions within 90 days of registration) stabilized at approximately 45%, suggesting that the vendor onboarding pipeline is healthy.

Platform Uptime and Reliability

DDoS (Distributed Denial of Service) attacks against darknet market onion services remained a persistent operational challenge. Markets with Tor v3 onion addresses and distributed infrastructure reported uptime averaging 94-97% over the quarter. Markets relying on single onion service instances without redundancy experienced more disruption. The adoption of multiple redundant v3 addresses as a standard practice continued to improve sector-wide reliability.

Statistics in this report are derived from publicly available monitoring sources, community-published data, and blockchain analysis of publicly known wallet addresses. All figures are estimates. This research is published for educational purposes only.